Fair School Funding Facts

PROPERTY TAX 101

The purpose of this narrative is to provide our readers with a better understanding of property tax basics, residential property tax liability distribution within a community, why school districts continue to levy taxes, and how to calculate residential school district property taxes. It will reference Ohio law and provide examples to illustrate the calculations, which support the narrative. The intent is to answer broad questions and educate the reader on how school district property taxes affect their individual real property tax liability.

Property Tax Basics

Local property taxes are taxes paid based upon land and building valuation located within the school district. Every owner of private and business property, including public utilities, must pay these taxes. County Auditors assess real estate taxes based upon 35% of the market value of a property. For example, an assessment of tax on property valued at $100,000 equates to $35,000 ($100,000 x .35 = $35,000).

The measurement or rate of local property tax is a mill. A mill is one thousandth of a dollar. According to the Ohio constitution, all local governments combined can levy only 10 mills without a vote of the people. Un-voted millage, or inside millage is inside the 10-mill limitation. Counties, school districts, municipalities, and/or townships of each taxing district divide the inside millage, of which Talawanda has 2.19 inside mills (general fund). Voters must approve all mills in excess of 10 mills (known as the “10 mill limitation”). Millage in excess of 10 mills, known as voted millage, or outside millage, cannot be collected without a majority vote from the voters in that specific district or community.

Click here to see the → Tax Rate Schedules for Butler County by Taxing District

Residential Property Tax Liability Distribution

House Bill 920, passed into law in 1976, limits the inflationary income of voted millage. County auditors reduce property tax millage correspondingly so that the real property tax of the average homeowner does not increase due to increased property valuation. This process creates a reduced tax rate or an effective millage rate that is less than the voted millage rate. The opposite occurs when property valuations decrease, the effective tax rate may increase to collect the original amount of tax passed by the voters. As a result, schools collect the same dollar amount that was previously approved by voters.

Why School Districts Continue to Levy Taxes

As previously stated, House Bill 920 restricts Ohio schools ability to collect inflationary increases on voted taxes. Voted mills are the primary source of income for our district, as it is in most school districts. House Bill 920 freezes a school district’s income on voted mills. As inflation increases property valuations and operating costs for schools, a school district’s revenue remains the same. Revenue increases will not occur for schools, except as a one-time increase for new construction and a small amount of revenue growth on inside mills. With income on voted mills frozen, school districts are forced to continually ask the local taxpayers for additional operating funds. This law forces most school districts to ask their local residents for more funds, on average, every three years.

Calculating Residential School District Property Taxes

Residential taxes are calculated by multiplying the market value of a homeowner’s property by the assessed valuations rate of 35 percent and then the effective millage rate of the school district (to maintain the original revenue voted in by the taxpayers) The state of Ohio applied homestead and rollback credits of 12.5% to voted millage tax rates prior to 2014. Voted millage in 2014 and after no longer receive that credit.

Click here to → Calculate your estimated property tax

Property taxes are an integral component of the revenue received by the Talawanda School District. The information provides the reader with general reference material as to how school district property taxes affect their individual real property tax liability and hopefully addresses some of the broader questions that you may have.

Want even more information on Property Taxes and/or Levies? Please click on the links below:

Property Taxation & School Funding

Understanding School Levies

Talawanda School District Current Voted (Outside) Millage

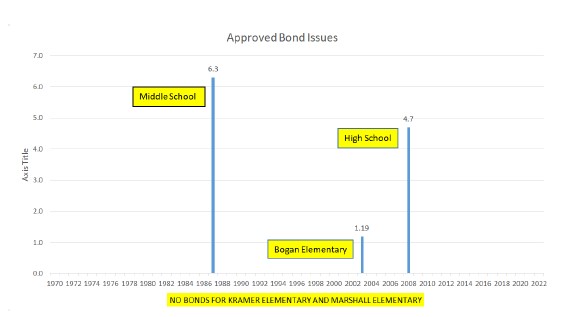

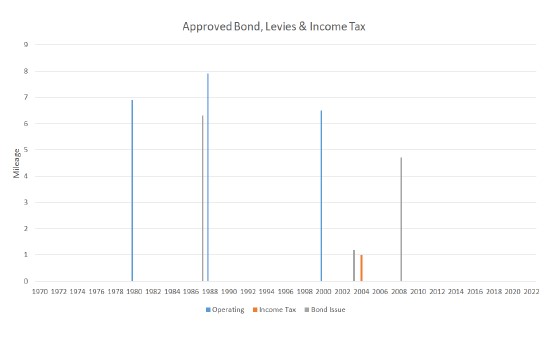

Our bond levies (1987, 2003 and 2008) have been utilized to construct three new buildings in our District. We have been able to construct two new buildings (Kramer and Marshall) utilizing our Permanent Improvement Fund in collaboration with the State of Ohio Facilities Construction Commission (OFCC).

School District Income Tax (SDIT)

The Ohio school district income tax generates revenue to support school districts who levy the tax. This tax is in addition to and separate from any federal, state, and city income or property taxes. Ohio school districts may enact a school district income tax with voter approval. Talawanda School District taxpayers approved a 1% SDIT in November of 2004, and it currently represents 22% of our annual revenue. As of January 2021, 208 school districts in our state impose an income tax.

Click here → To learn more on Ohio School District Income Tax

If you want to review the Ohio School District Income Tax FAQs

Reference Materials Used:

Butler County Auditor, Ohio Department of Taxation, NAPLS, Investopedia

School District Fund Accounting

Talawanda School District uses funds to maintain its financial records during the fiscal year. A fund is defined as a “fiscal and accounting entity with a self-balancing set of accounts”. There are three categories of funds: governmental, proprietary and fiduciary.

Governmental Funds

Most of the District’s activities are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at the end of the fiscal year available for spending in the future periods. These funds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted into cash. The governmental fund statements provide a detailed short-term view of the District’s general government operations and the basic services it provides. Governmental Fund information helps you determine whether there are more or fewer financial resources that can be spent in the near future to finance educational programs.

The District’s major governmental funds are the general fund, special revenue, debt service and capital project funds. The general fund is used to account for and report all financial resources not accounted for and reported in another fund. The general fund balance is available for any purpose provided it is expended or transferred according to the general laws of Ohio.

General Fund (001): The general fund is what is utilized in our five year forecast.

Other governmental funds of the District include:

Special Revenue Funds: Special revenue funds are used to account for and report the proceeds of specific revenue sources that are restricted or committed to an expenditure for specified purposes other than debt service or capital projects.

Public School Support/Principal’s Funds (018)

TMS and THS Athletic Funds (300)

State Grants (401 – 499)

Federal Grants (507 – 599)

Debt Service Funds: Debt service funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for principal and interest.

Bogan and THS Bonds (002)

The District’s debt service fund is used to account all debt activity except the debt associated with the construction of Kramer and Marshall Elementary which is accounted for in a capital project fund (003 Fund).

Capital Projects Funds: Capital projects funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays (has a life span of 3+ years), including the acquisition or construction of capital facilities and other capital assets.

Permanent Improvement (003)

Building Construction (004)

Classroom Facilities-OFCC (010)

Proprietary Funds

Proprietary funds focus on the determination of operating income/loss, changes in net position, financial position and cash flows and are classified as either enterprise or internal service.

Enterprise funds – Enterprise funds may be used to account for any activity for which a fee is charged to external users for goods or services. The District currently has two enterprise funds.

Food Services (006) and Classroom Supplies/Materials (009)

Internal service funds – Internal service funds are used to account for the financing of goods or services provided by one department or agency to other departments or agencies of the District or to other governments, on a cost-reimbursement basis. The District has no internal service funds.

Fiduciary Funds

Fiduciary fund reporting focuses on net position and changes in net position. The fiduciary fund category is split into four classifications: pension trust funds, investment trust funds, private-purpose trust funds and agency funds. Trust funds are used to account for assets held by the District under a trust agreement for individuals, private organizations, or other governments and are therefore not available to support the District’s own programs. Agency funds are custodial in nature (assets equal liabilities) and do not involve measurement of results of operations. The District’s agency funds account for our unclaimed funds from expired disbursement checks and for student activities and amounts held for individuals and organizations.

TSD Unclaimed Funds (022) and Student Managed Activity Funds (200)

Basis of accounting determines when transactions are recorded in the financial records and reported on the financial statements. Governmental funds use the modified accrual basis of accounting. Proprietary funds use the accrual basis of accounting.

Budgetary Basis of Accounting

The budgetary process is prescribed by provisions of the Ohio Revised Code and entails the preparation of budgetary documents within an established timetable. The major documents prepared are the tax budget, the certificate of estimated resources, and the appropriation resolution, all of which are prepared on the budgetary basis of accounting.

The certificate of estimated resources and the appropriations resolution are subject to amendment throughout the year with the legal restriction that appropriations cannot exceed estimated resources, as certified by the Butler County Auditor. All funds, other than agency funds, are legally required to be budgeted and appropriated. The primary level of budgetary control is at the fund level of expenditures. Any budgetary modifications at this level may only be made by resolution of the Board of Education. Although the legal level of control has been established at the fund level of expenditures, the District has elected to present the budgetary statement for the general fund at the fund and function level of expenditures in the basic financial statements.

Advances in and out are not required to be budgeted since they represent a temporary cash flow resource and are intended to be repaid.

Fiscal Year Budget Planning Calendar

On or before January 15

Tax Budget for July 1 of following fiscal year is approved by the board of education.

On or before January 20

The board-adopted budget is filed with the County Budget Commission for review and approval.

February prior fiscal year

Allocations for each building and department are submitted to the administrators to allocate among their funds based on department/building budget planning meetings.

On or before April 15

Building and department administrators submit proposed building/department budgets to treasurer and superintendent.

On or before May 30

Board of education adopts updated Five-Year General Operating Fund Forecast for the fiscal year that started the previous July.

On or before July 1

Temporary appropriations are approved by the board of education to remain in effect until no later than October 1.

On or before September 30

The board of education approves the permanent appropriations (annual budget) for the fiscal year that started July 1.

On or before November 30

Board of education adopts Five-Year General Operating Fund Forecast for the fiscal year that started July 1.

Revenues/Receipts

On the modified accrual basis of accounting, revenue is recognized at the time the funds are received and posted to the District’s accounting system. The measurement focus of governmental fund accounting is on increases in net financial resources (revenues). Revenues are generally recognized in the accounting period in which the inflow of cash is received. Allocations of assets, such receivables and inventories, are not recognized in the budgetary statements of the governmental fund.

Expenses/Expenditures

On the accrual basis of accounting, expenses are recognized at the time they are incurred. The measurement focus of governmental fund accounting is on decreases in net financial resources (expenditures) rather than expenses. Expenditures are generally recognized in the accounting period in which the related fund liability is incurred, if measurable. Allocations of cost, such as depreciation and amortization, are not recognized in governmental funds.

Other Financing Sources and Uses

Inflows and outflows of funds recorded under this category are not considered revenue or expenditures in the budgetary statements. Rather they are provided separately in the budgetary statements to identify the effect the transaction(s) have on the fund balance outside of general operating transactions.

District Legal Status

Statutorily, the District operates under standards prescribed by the Ohio State Board of Education as provided in Division (D) Section 3301.07 and Section 119.01 of the Ohio Revised Code, to provide educational services prescribed by the state and/or federal agencies. An elected five-member Board of Education serves as the taxing authority and policy maker for the District. The Board adopts the annual operating budget, tax budget, and approves all expenditures of District tax monies. The Superintendent is the Chief Executive Officer of the District, responsible to the Board for total educational and support operations. The Treasurer is the Chief Financial Officer of the District, responsible to the Board for maintaining all financial records, issuing warrants in payment of liabilities incurred by the District, acting as custodian of all District funds, and investing idle funds as permitted by Ohio law.

Reference Materials Used:

Uniform School Accounting System